Hedge fun

The automobile industry does it. The airline industry does it too. American wine importers need to use currency hedging to prevent price rises and protect their profits.

Porsche, the luxury auto maker, reported a rise in profits for the first-half of their fiscal year. While this alone raised eyebrows because of global economic sluggishness, the real surprise was that there was any profit at all for the German company since just about half of its sales came from the US market. After all, the dollar’s sharp decline against the euro should have eaten most of the profits. But it did not. Why?

Management predicted the dollar decline and bought a currency hedge through 2006-7. This hedge is not an ornament of the manicured lawn at the Stuttgart HQ, but rather a financial strategy that limits the risk of currency fluctuations. The hedging program saved the corporation’s profits—and protected the leather-loafered American consumer from having to pay higher prices for the product.

Hedging is common in industries with volatile markets. Continental Airlines’ recent profits were hurt because they did not hedge their fuel costs the way most airlines do. Starbucks hedges the risk of a coffee price rise. Some heating oil companies even offer consumers the right to lock in their winter fuel bill at summer prices.

Hedges, once the exclusive domain of investment bankers, have now gone mainstream. Hedging provides a firm the opportunity to manage risk, often at a reasonable price (and there are even some “zero cost” options). In the wine industry, if American importers anticipate a decline in the dollar, which would raise their costs of buying wine overseas, they can buy the foreign currency at today’s prices in what is called the spot market. But that would tie up a lot of capital to simply buy, say, one million euros today. A lower cost strategy is to buy cheap options on one million euros at today’s prices. This provides the importer insurance against a decline of the dollar. And a similar strategy can even be set up to protect against a rise in the dollar too.

Wine needs currency hedging more than other consumer products.

Car producers can hedge their currency risk by moving production into the consuming countries as BMW did by opening a plant in South Carolina. But wine producers cannot shift production. Wine from Burgundy cannot be produced in Bangalore. That makes wine extremely vulnerable to currency fluctuations.

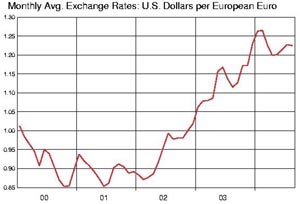

As the dollar has dropped sharply over the past two years, particularly against the euro and the Australian dollar (see chart below), the two main currencies of American wine imports, wine consumers have had to suffer a rise in wine prices on the retailers’ shelves.

Wine from Burgundy cannot be produced in Bangalore.

Futures for the wines of the Bordeaux 2003 vintage have more than doubled from the prior year for many of the top chateaus. Granted, the extreme heat of the growing season led to some rave reviews for the vintage. But even other, more humble wines from other region of the euro-zone that used to sell for under $10 now are pushing $13.

Passing the cost of currency fluctuations on to the consumer is but one strategy for an importer. One importer told me that his sales had doubled recently while his profits remained flat because he refused to raise prices to the consumer. Instead of simply buying the currency in the spot market, just think how much profit he could have made with a hedging program! He could even have lowered prices while his competitors raised them.

Wine consumers are already accustomed to producer greed driving up prices. The financial bumbling of importers should not further add to the tab. American wine importers would do well to seize this current pullback in the dollar to purchase some protection against another run on the dollar. (With large deficits in trade and the federal budget, it’s not too difficult to imagine the dollar losing ground again.) That way squeezing or squabbling with producers about price can be avoided and the price can remain stable to the consumer. Then the saved profits could help the importer’s bottom line—or even be passed on to the consumer in the form of lower prices!

FX rates at publication (8/24/04)

euro/dollar: 1.2099

US dollar/Australian dollar: 1.4156

image sources:

1) Porsche

2) www.n-tv.de/5204475.html

3) & 4) http://fx.sauder.ubc.ca/plot.html

On September 3rd, 2008 at 6:57 am ,Has the wine inflation beast been slain? | Dr Vino's wine blog wrote:

[…] cause consumers to trade down for cheaper bottles so they may hold the line on price increases (or hedge their risk if they think the current dollar rally is but a head fake). So maybe we’ll see no more price […]

On October 16th, 2008 at 9:21 pm ,Value vino list number eleven | Dr Vino's wine blog wrote:

[…] out quite well and they are generally good values. (It’s not that their importers have hedged the currency risk successfully; they’re just cheap with improving quality) This producer is […]